Coincido en que la economía no es "tan simple", pero compararme la década perdida japonesa con la Gran Depresión y otras similares de cuando el patrón oro tiene delito.Por mucho que se repita, no se va a poder probar ciertos mantras:

Even before the Great Depression, downturns were typically much deeper and longer than they are today (see right-hand chart). One reason why recessions have become milder is higher government spending.

El caso japonés muestra, de manera impresionante, la falsedad de esta afirmacion. Es más, en cuando la recesion llega a alargarse en el tiempo, la politica del gasto público tiene efectos prociclicos. Porque al parecer, la economia no es tan simple, como inyectar gasoil a aire comprimida al 5% de su volumen normal, causa necesariamente una explosion espontanea...:

Y luego, las deudas hay que pagarlas.

(Para quien lo interesa, el conforero Sylar tiene por allí un magnifico post sobre la politica economica japonesa en las últimas decadas.)

POR FAVOR! QUE LA GRAN DEPRESIÓN SUPUSO UNA CAIDA DEL PIB NOMINAL DEL 50 PORCIEN, Y DEL 30 PORCIEN REAL!

Japón:

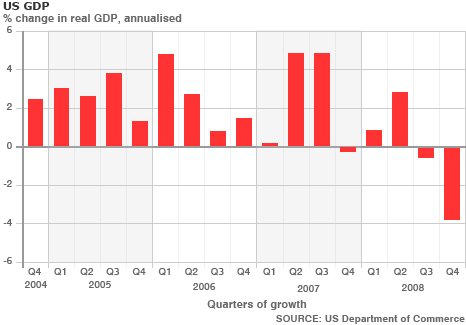

EE.UU:

También podemos hablar de la recesión de 1957, y de todas las que se os ocurran... aqui hay un buen listado:

http://en.wikipedia.org/wiki/List_of_recessions_in_the_United_States

Así que ya basta de mentiras auroinómanas!

Última edición: