visillófilas pepitófagas

Madmaxista

- Desde

- 6 Oct 2008

- Mensajes

- 3.138

- Reputación

- 9.615

A Housing Update

If you read the headlines the last few days you would think that the housing market has turned. Mostly they read something like "Home Sales Rise 0.3%," and of course the reflexive bulls started talking about green shoots and a bottom in housing. And while someday we will actually have a bottom in housing, it will not be this month. It has been awhile since we have looked at the housing market, and it is time to review.

First. Of course home sales rose. It is April. Look at the graph below. It is the time of the year when home sales rise. And 0.3%? Really? The margin of error is close to plus or minus 10% or so, so 0.3% is a meaningless number. It will be revised. Who knows which way? I don't. (I am on the plane so I cannot access the exact margin of error, but 10% is not that far off.)

My main thesis since 2006 has been that the housing market was in a bubble that would burst. We built something like an extra 3 million homes over trend growth, and those homes are going to have to be absorbed in the normal way, through growth of population and the economy. We "need" about 1 million new homes a year to take care of population growth and demand. Further, we have cut off home availability to buyers who are in the subprime category, whereas during the boom you simply had to have a pulse, even a lying pulse, to get a home for which you did not have a chance of actually paying the mortgage.

The earliest we see a real bottom to housing is late 2010 or 2011. By real bottom I am talking about housing values in general being to rise (assuming we do not visit scenario one and have significant inflation.) There is nothing that can be done about that. We have to work through the excess capacity. (More later on that below.)

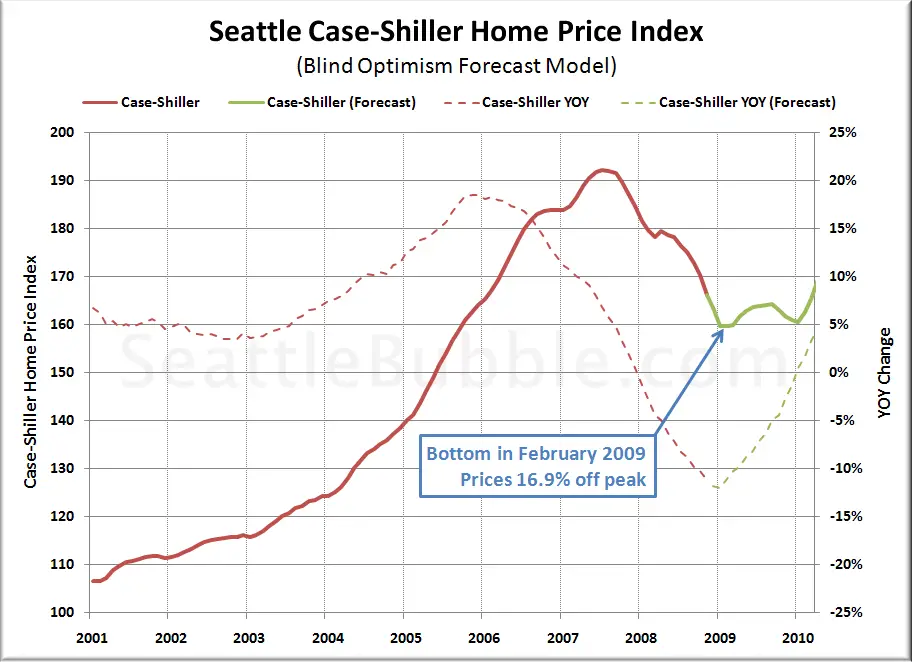

We had the Case-Shiller home price data come out this week. Home prices are still in free fall. They are down almost 19% year over year and 32% from their 2006 highs (see chart below). If we get back to the long-term price growth trend, we would see another average 10% drop; and as prices tend to overshoot on the upside and the downside, in some markets they could fall even further.

Yet there is hope that we will not see a fall below trend. Housing in many areas is starting to once again become affordable (see chart from Moody's below) to more and more Americans and even first-time home buyers. The cure for the housing crisis is actually lower prices, as that brings more and more potential home buyers into the market. While housing sales are still quite depressed, what are selling are homes in foreclosure, as buyers perceive that there are bargains. And they are right.

On the negative side, the supply of homes available for sale is again rising, as more and more foreclosures come onto the market. And as we will see, this foreclosure trend is going to slow down soon. (Thanks to Greg Weldon at Weldon's Money Monitor, Weldon's ETF Playbook, Weldon's Metal Monitor from Weldon Financial Publishing, Global Macro Research for the chart.)

Notice in the above chart that the supply of homes for sale is over ten months. But that average can be misleading. If you are in Florida, I read recently that in many areas it is over 40 months. And that is for homes that can be financed with government-sponsored "conforming loans," typically up to $719,000. But what if your home cost more than that? National Association of Realtors chief economist Lawrence Yun said that the supply of existing homes for sale over $750,000 has reached a forty-month supply.

Diana Olick, the very on-top-of-it CNBC real estate reporter, had the amowing to say (emphasis mine).

"That's going to miccionan a new phase of the current housing recession. So far we've seen the 'correction' of a boom market that was driven by faulty, exotic loan products, investors looking to make a quick buck, and average Americans using their homes as ATMs. Now the losses are being driven by traditional economic factors and by sweeping price drops across the nation.

"Yesterday Fitch ratings estimated that up to 75 percent of the modifications now being done through the administration's Making Home Affordable program will re-default in six months to a year. I'm not talking about the old modifications, which were largely repayment plans that could actually raise monthly payments. I'm talking about the new mods, which lower monthly payments to 31 percent of a person's income. I couldn't understand Fitch's reasoning, so I called them.

"Diane Pendley, managing director at Fitch, said the problem is not on that "front-end" ratio, but on the back end, which is all of the borrowers other debt (credit cards, car loans, student loans, etc.). She said that in talking with servicers, she's hearing other debt is so high that most of today's troubled borrowers cannot afford any loan payment at all, even at a very modest debt-to-income ratio. 'Just getting the house payment done doesn't miccionan their lifestyle is sustainable,' she said.

"Another problem is that with home prices continuing to fall, more and more borrowers, who are essentially just renting their mortgages now because they will never see any home equity, are walking away. Even if the mortgage payment is low, the property taxes and home maintenance costs are padding that payment, and without an upside to the investment, there's simply no reason to pay. Suffice it to say, the foreclosure crisis, on the high and low ends, is not getting any better."

And it gets worse.

More Prime Foreclosures In Our Future

The Mortgage Bankers Association noted that a record 12%, or 1 in 8 homeowners, in the US are now behind on their payments or in foreclosure. 10.6% of the mortgages in Florida are now somewhere in the process of actual foreclosure. (My seatmate here on the flight says the prices on the condos where he lives are now back to 1998 levels. It would be scary, he said, if you had to sell. There are new developments that only have 10% actual occupancy, as the bulk of the condos were bought for speculation. Now those 10% of buyers are having to shoulder all the fees for upkeep. Nobody will buy, because the upkeep costs can be more than the mortgage. It is a vicious cycle.)

In Nevada foreclosures are 7.8%, Arizona 5.6%, and California 5.2%. 25% of subprime loans are now in foreclosure, 14% of FHA (government, taxpayer-guaranteed) loans and a growing 6% of all prime loans are now in foreclosure. (Note: the seasonal adjustments may overstate the actual numbers, as we are in new territory in terms of actual foreclosures.) Quoting from the MBA press release:

"In looking at these numbers, it is important to focus on what has changed as well what continue to be the key drivers of foreclosures. What has changed is the shifting of the problem somewhat away from the subprime and option ARM/Alt-A loans to the prime fixed-rate loans. The foreclosure rate on prime fixed-rate loans has doubled in the last year, and, for the first time since the rapid growth of subprime lending, prime fixed-rate loans now represent the largest share of new foreclosures. In addition, almost half of the overall increase in foreclosure starts we saw in the first quarter was due to the increase in prime fixed-rate loans." (emphasis mine)

How could so many prime loans be in foreclosure? These were people with good credit and jobs. The answer is the very deep and lengthy recession, coupled with high and rising unemployment. The number of foreclosures will not abate until unemployment starts to fall. And even optimistic forecasts assume unemployment will keep rising into 2010. As I have written for a long time, I think it is quite likely that we will see unemployment rise to over 10%. When I first wrote that a few years ago, many called me just another doom and gloom guy. Now, many think I am Pollyanna. Such is the life of those who believe in Muddle Through.

For those who think the end of the recession will be like all past recessions, the problems in the housing market should make for serious concern. As we will see on Monday in my Outside the Box, the average homeowner with a mortgage has very little, if any, equity. There is little room for home equity withdrawals -- if banks were lending. And recent data shows a very serious and un-American-like drop in credit card borrowing. US consumers are retrenching, and global trade figures echo that.

We are in for a slow, Muddle Through recovery, with the real potential to slip back into recession when the tax increases hit. Stay tuned.

----------------------

John Mauldin, Best-Selling author and recognized financial expert, is also editor of the free Thoughts From the Frontline that goes to over 1 million readers each week. For more information on John or his FREE weekly economic letter go to: Thoughts from the Frontline

If you read the headlines the last few days you would think that the housing market has turned. Mostly they read something like "Home Sales Rise 0.3%," and of course the reflexive bulls started talking about green shoots and a bottom in housing. And while someday we will actually have a bottom in housing, it will not be this month. It has been awhile since we have looked at the housing market, and it is time to review.

First. Of course home sales rose. It is April. Look at the graph below. It is the time of the year when home sales rise. And 0.3%? Really? The margin of error is close to plus or minus 10% or so, so 0.3% is a meaningless number. It will be revised. Who knows which way? I don't. (I am on the plane so I cannot access the exact margin of error, but 10% is not that far off.)

My main thesis since 2006 has been that the housing market was in a bubble that would burst. We built something like an extra 3 million homes over trend growth, and those homes are going to have to be absorbed in the normal way, through growth of population and the economy. We "need" about 1 million new homes a year to take care of population growth and demand. Further, we have cut off home availability to buyers who are in the subprime category, whereas during the boom you simply had to have a pulse, even a lying pulse, to get a home for which you did not have a chance of actually paying the mortgage.

The earliest we see a real bottom to housing is late 2010 or 2011. By real bottom I am talking about housing values in general being to rise (assuming we do not visit scenario one and have significant inflation.) There is nothing that can be done about that. We have to work through the excess capacity. (More later on that below.)

We had the Case-Shiller home price data come out this week. Home prices are still in free fall. They are down almost 19% year over year and 32% from their 2006 highs (see chart below). If we get back to the long-term price growth trend, we would see another average 10% drop; and as prices tend to overshoot on the upside and the downside, in some markets they could fall even further.

Yet there is hope that we will not see a fall below trend. Housing in many areas is starting to once again become affordable (see chart from Moody's below) to more and more Americans and even first-time home buyers. The cure for the housing crisis is actually lower prices, as that brings more and more potential home buyers into the market. While housing sales are still quite depressed, what are selling are homes in foreclosure, as buyers perceive that there are bargains. And they are right.

On the negative side, the supply of homes available for sale is again rising, as more and more foreclosures come onto the market. And as we will see, this foreclosure trend is going to slow down soon. (Thanks to Greg Weldon at Weldon's Money Monitor, Weldon's ETF Playbook, Weldon's Metal Monitor from Weldon Financial Publishing, Global Macro Research for the chart.)

Notice in the above chart that the supply of homes for sale is over ten months. But that average can be misleading. If you are in Florida, I read recently that in many areas it is over 40 months. And that is for homes that can be financed with government-sponsored "conforming loans," typically up to $719,000. But what if your home cost more than that? National Association of Realtors chief economist Lawrence Yun said that the supply of existing homes for sale over $750,000 has reached a forty-month supply.

Diana Olick, the very on-top-of-it CNBC real estate reporter, had the amowing to say (emphasis mine).

"That's going to miccionan a new phase of the current housing recession. So far we've seen the 'correction' of a boom market that was driven by faulty, exotic loan products, investors looking to make a quick buck, and average Americans using their homes as ATMs. Now the losses are being driven by traditional economic factors and by sweeping price drops across the nation.

"Yesterday Fitch ratings estimated that up to 75 percent of the modifications now being done through the administration's Making Home Affordable program will re-default in six months to a year. I'm not talking about the old modifications, which were largely repayment plans that could actually raise monthly payments. I'm talking about the new mods, which lower monthly payments to 31 percent of a person's income. I couldn't understand Fitch's reasoning, so I called them.

"Diane Pendley, managing director at Fitch, said the problem is not on that "front-end" ratio, but on the back end, which is all of the borrowers other debt (credit cards, car loans, student loans, etc.). She said that in talking with servicers, she's hearing other debt is so high that most of today's troubled borrowers cannot afford any loan payment at all, even at a very modest debt-to-income ratio. 'Just getting the house payment done doesn't miccionan their lifestyle is sustainable,' she said.

"Another problem is that with home prices continuing to fall, more and more borrowers, who are essentially just renting their mortgages now because they will never see any home equity, are walking away. Even if the mortgage payment is low, the property taxes and home maintenance costs are padding that payment, and without an upside to the investment, there's simply no reason to pay. Suffice it to say, the foreclosure crisis, on the high and low ends, is not getting any better."

And it gets worse.

More Prime Foreclosures In Our Future

The Mortgage Bankers Association noted that a record 12%, or 1 in 8 homeowners, in the US are now behind on their payments or in foreclosure. 10.6% of the mortgages in Florida are now somewhere in the process of actual foreclosure. (My seatmate here on the flight says the prices on the condos where he lives are now back to 1998 levels. It would be scary, he said, if you had to sell. There are new developments that only have 10% actual occupancy, as the bulk of the condos were bought for speculation. Now those 10% of buyers are having to shoulder all the fees for upkeep. Nobody will buy, because the upkeep costs can be more than the mortgage. It is a vicious cycle.)

In Nevada foreclosures are 7.8%, Arizona 5.6%, and California 5.2%. 25% of subprime loans are now in foreclosure, 14% of FHA (government, taxpayer-guaranteed) loans and a growing 6% of all prime loans are now in foreclosure. (Note: the seasonal adjustments may overstate the actual numbers, as we are in new territory in terms of actual foreclosures.) Quoting from the MBA press release:

"In looking at these numbers, it is important to focus on what has changed as well what continue to be the key drivers of foreclosures. What has changed is the shifting of the problem somewhat away from the subprime and option ARM/Alt-A loans to the prime fixed-rate loans. The foreclosure rate on prime fixed-rate loans has doubled in the last year, and, for the first time since the rapid growth of subprime lending, prime fixed-rate loans now represent the largest share of new foreclosures. In addition, almost half of the overall increase in foreclosure starts we saw in the first quarter was due to the increase in prime fixed-rate loans." (emphasis mine)

How could so many prime loans be in foreclosure? These were people with good credit and jobs. The answer is the very deep and lengthy recession, coupled with high and rising unemployment. The number of foreclosures will not abate until unemployment starts to fall. And even optimistic forecasts assume unemployment will keep rising into 2010. As I have written for a long time, I think it is quite likely that we will see unemployment rise to over 10%. When I first wrote that a few years ago, many called me just another doom and gloom guy. Now, many think I am Pollyanna. Such is the life of those who believe in Muddle Through.

For those who think the end of the recession will be like all past recessions, the problems in the housing market should make for serious concern. As we will see on Monday in my Outside the Box, the average homeowner with a mortgage has very little, if any, equity. There is little room for home equity withdrawals -- if banks were lending. And recent data shows a very serious and un-American-like drop in credit card borrowing. US consumers are retrenching, and global trade figures echo that.

We are in for a slow, Muddle Through recovery, with the real potential to slip back into recession when the tax increases hit. Stay tuned.

----------------------

John Mauldin, Best-Selling author and recognized financial expert, is also editor of the free Thoughts From the Frontline that goes to over 1 million readers each week. For more information on John or his FREE weekly economic letter go to: Thoughts from the Frontline

")